Continual learning without forgetting for object detector in streaming data Market Growth Analysis, Dynamics, Key Players and Innovations, Outlook and Forecast 2026-2034

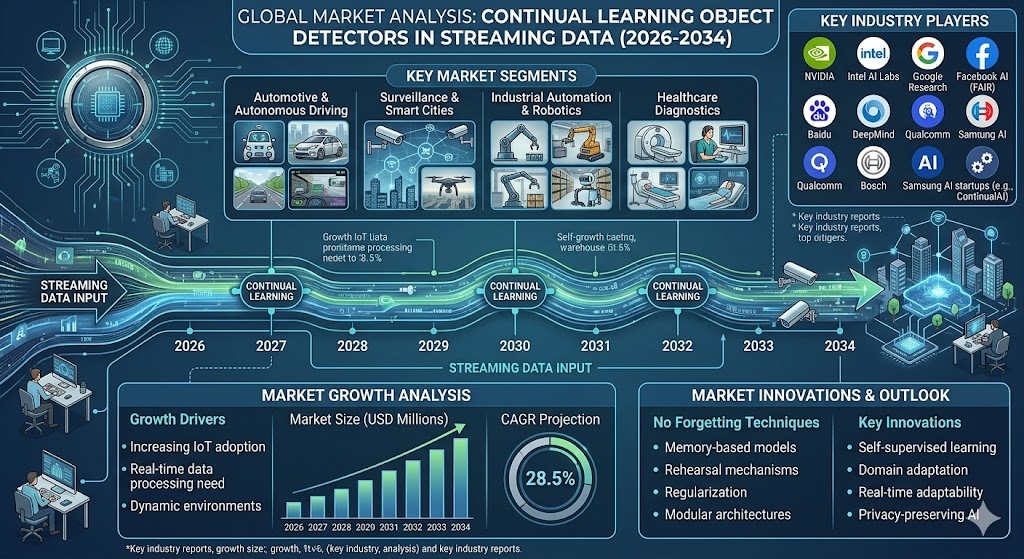

The global Continual Learning for Object Detection in Streaming Data Market is on a trajectory of rapid expansion, driven by escalating demand for AI‑enabled edge analytics, autonomous systems, and real‑time visual intelligence across diverse verticals. Industry analysts project a strong compound annual growth rate (CAGR) throughout the forecast horizon, reflecting the strategic importance of models that can learn from continuous streams without forgetting previously acquired knowledge.

Continual learning, also known as incremental or lifelong learning, empowers object detectors to adapt to evolving environments-such as changing lighting conditions, new object classes, or shifting domain characteristics-while preserving the accuracy of earlier detections. This capability is increasingly vital for applications that cannot afford costly model re‑training cycles, data‑center bandwidth limitations, or downtime associated with legacy model updates.

Download FREE Sample Report:

Continual learning without forgetting for object detector in streaming data Market - View in Detailed Research Report

Why Continual Learning is Becoming a Cornerstone of Modern AI Deployments

Traditional deep‑learning pipelines rely on a static training‑once‑deploy‑forever paradigm, which is ill‑suited for environments where data distributions drift over time. In video surveillance, for instance, new vehicle models, fashion trends, or seasonal decorations appear regularly, demanding that detection systems stay current without erasing the knowledge of previously seen objects. In autonomous navigation, road‑sign updates, construction zones, and weather‑induced visual variations require on‑the‑fly model adaptation. Continual learning addresses these challenges by integrating mechanisms such as elastic‑weight consolidation, rehearsal buffers, and knowledge distillation, enabling models to refine their parameters incrementally while mitigating catastrophic forgetting.

Key Growth Drivers

1. Explosion of Edge‑Centric AI Hardware – The proliferation of AI‑accelerated edge processors (e.g., NVIDIA Jetson, Intel Movidius, Qualcomm Snapdragon) provides the computational bandwidth needed for on‑device model updates. These platforms are designed with low‑power envelopes and dedicated tensor cores that support dynamic weight adjustments in real time.

2. Regulatory and Privacy Pressures – Data‑locality regulations in Europe (GDPR), China (Cybersecurity Law), and emerging frameworks in the United States increasingly mandate that sensitive visual data remain on‑device. Continual learning enables compliance by eliminating the need to transmit raw video streams to centralized servers for retraining.

3. Cost Efficiency in Model Maintenance – Enterprises are recognizing that frequent full‑scale retraining incurs substantial compute, storage, and human‑resource expenses. Incremental learning reduces overall total cost of ownership (TCO) by leveraging existing model weights and limiting data movement.

4. Demand from High‑Impact Verticals – Autonomous vehicles, smart‑city surveillance, industrial robotics, retail analytics, and telemedicine each require detection systems that stay current with minimal latency. The market’s breadth across these sectors fuels sustained growth.

5. Advancements in Algorithmic Research – Academic breakthroughs in memory‑efficient replay buffers, meta‑learning based plasticity, and federated continual learning are rapidly transitioning into commercial SDKs, widening the pool of developers able to implement these techniques.

Market Segmentation: Deployment Models and End‑User Applications

The market can be segmented along two principal dimensions, each reflecting distinct adoption pathways and revenue streams.

By Deployment Model

- Edge‑Only Solutions – Embedded AI chips and micro‑controllers that perform on‑device updates without cloud reliance.

- Cloud‑Assisted Platforms – Hybrid architectures where streaming data is pre‑processed at the edge, with periodic weight refinement performed in the cloud and pushed back to devices.

- Fully Managed SaaS – Subscription‑based services offering continual‑learning pipelines as a turnkey solution, often bundled with data annotation and model‑monitoring dashboards.

By End‑User Application

- Smart‑City Surveillance & Public Safety

- Autonomous Driving & Advanced Driver‑Assistance Systems (ADAS)

- Industrial Robotics & Predictive Maintenance

- Retail Analytics & Shelf Monitoring

- Healthcare Imaging & Remote Diagnosis

- Agricultural Monitoring & Precision Farming

- Augmented & Virtual Reality (AR/VR) Headsets

- Drone‑Based Inspection & Mapping

Regional Outlook

North America – The United States leads in R&D investment for edge AI and hosts a concentration of tech giants that are integrating continual‑learning modules into their developer ecosystems. Federal funding for autonomous vehicle testbeds and smart‑city pilots further accelerates market uptake.

Europe – Strong regulatory frameworks around data privacy coupled with a mature automotive sector make Europe a hotbed for privacy‑preserving continual learning. Initiatives such as the European AI Alliance promote standards for on‑device learning, fostering cross‑border collaborations.

Asia‑Pacific – The region accounts for the majority of edge‑AI hardware manufacturing, with China, Japan, South Korea, and India investing heavily in AI‑enabled IoT. High‑density urban environments drive demand for real‑time surveillance and traffic‑management solutions that rely on continual learning.

Middle East & Africa – Emerging smart‑city projects in the United Arab Emirates, Saudi Arabia, and South Africa are beginning to adopt edge AI platforms, creating early‑stage opportunities for continual‑learning technologies.

Technological Trends Shaping the Market

1. Elastic‑Weight Consolidation (EWC) – Regularization techniques that protect important weights, enabling models to accommodate new data while retaining historical performance.

2. Replay‑Buffer Strategies – Selective storage of representative samples from previous tasks to rehearse and mitigate forgetting, increasingly optimized for memory‑constrained devices.

3. Knowledge Distillation for Continual Learning – Teacher‑student frameworks where a compact student model inherits knowledge from a larger teacher without direct access to all past data.

4. Federated Continual Learning – Decentralized training across multiple edge nodes, preserving data locality while collectively improving model robustness.

5. Hardware‑Software Co‑Design – ASICs and neuromorphic chips that embed forgetting‑free modules directly into the silicon, reducing latency and power consumption for on‑device updates.

Competitive Landscape

COMPETITIVE LANDSCAPE

Key Industry Players

Continual Learning for Object Detection: Market Competitive Landscape

The market is dominated by a handful of technology giants that have integrated continual‑learning pipelines directly into their AI‑accelerated hardware and SDKs. NVIDIA leads with its Jetson edge modules and the TensorRT Inference Server, offering elastic‑weight‑consolidation libraries that enable real‑time model updates without sacrificing legacy detection accuracy. Intel follows closely, leveraging the OpenVINO toolkit and Movidius Myriad chips to embed replay‑buffer strategies in edge deployments for smart‑city surveillance and autonomous navigation. Apple’s on‑device Core ML framework extends these techniques to iOS devices, emphasizing privacy‑preserving incremental learning. OpenAI, while primarily known for generative models, contributes research‑grade regularization methods that are being adopted by enterprise customers. Together, these leaders shape a market structure where hardware‑software co‑design and proprietary SDKs drive the majority of revenue, while collaborative standards such as ONNX continue to lower entry barriers for downstream adopters.

Beyond the headline names, several niche but highly innovative players are sharpening the competitive edge of the sector. Google DeepMind and Meta FAIR invest heavily in open‑source continual‑learning algorithms that target large‑scale visual datasets, feeding the research pipeline for many startups. Samsung and Qualcomm focus on low‑power ASICs that embed forgetting‑free modules for wearables and AR glasses. Bosch and Huawei apply the technology to industrial IoT and smart‑retail platforms, respectively, often partnering with regional system integrators. Emerging specialists such as SenseTime, Tesla Autopilot, IBM Research, and Amazon Web Services provide cloud‑native services and domain‑specific datasets that enable rapid model refresh cycles across verticals ranging from autonomous driving to retail analytics.

List of Key Continual Learning for Object Detector Companies Profiled

-

Apple Inc.

-

OpenAI

-

Google DeepMind

-

Meta AI (FAIR)

-

Samsung Electronics

-

Qualcomm Technologies

-

Bosch Security Systems

-

Huawei Technologies

-

SenseTime Group Ltd.

-

Tesla, Inc.

-

IBM Research

-

Microsoft Azure AI

Strategic Initiatives Observed Across the Landscape

- Integration of on‑device continual‑learning modules into existing SDKs to reduce time‑to‑market for developers.

- Partnerships with automotive OEMs and smart‑city consortia to embed forgetting‑free detection in safety‑critical deployments.

- Open‑source contributions (e.g., TensorFlow Lite, PyTorch Mobile) that democratize access to rehearsal‑based algorithms.

- Acquisitions of niche startups specializing in memory‑efficient replay buffers or neuromorphic processors.

- Investment in benchmark datasets that reflect real‑world distribution shifts, such as continuously annotated traffic‑camera feeds.

Emerging Opportunities and Market Outlook (2026‑2034)

The convergence of several macro‑trends positions the continual‑learning for object detection market for sustained expansion through 2034. Autonomous vehicle manufacturers increasingly require on‑board perception systems that can incorporate firmware updates without extensive off‑line retraining, a direct use case for forgetting‑free models. In retail, real‑time shelf‑stock detection benefits from incremental learning that adapts to new product packaging without re‑labeling entire datasets. Healthcare imaging platforms are exploring continual learning to accommodate novel disease‑pattern annotations while preserving diagnostic accuracy for previously seen cases.

Furthermore, the rise of 5G and upcoming 6G networks reduces latency for cloud‑assisted hybrid pipelines, enabling more frequent weight synchronizations between edge and central servers. This network evolution, combined with energy‑efficient ASICs, is expected to lower the total cost of continual‑learning deployments, making the technology attractive for mid‑size enterprises.

Analysts forecast that by the end of the 2034 horizon, the market will command multi‑billion‑dollar revenues, with hardware‑software co‑design solutions capturing the largest share, followed by SaaS‑based platforms that offer end‑to‑end model‑lifecycle management.

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us