Optical Transceivers Market, Trends, Business Strategies 2025-2032

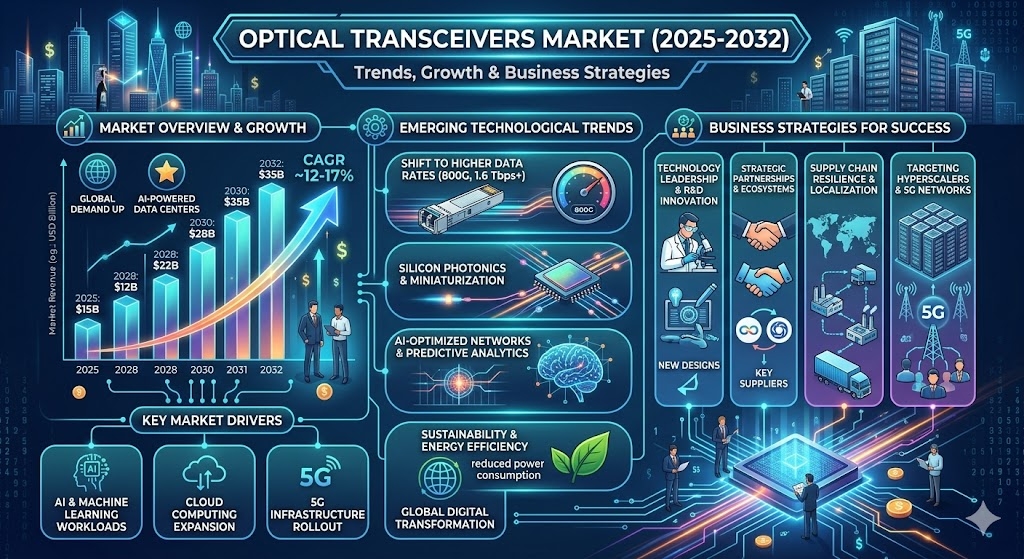

The global Optical Transceivers Market continues to gain momentum as data‑intensive applications, 5G roll‑outs, and the rise of hyperscale cloud infrastructures accelerate demand for higher‑speed, more reliable optical connectivity solutions. Industry analysts note that the market is being reshaped by rapid advances in modulation formats, integration of silicon photonics, and the relentless push for greater bandwidth per fiber. Although precise valuation figures vary across forecasts, the consensus underscores a robust growth trajectory that will sustain investment and innovation across the value chain through 2032.

Optical transceivers serve as the critical bridge between electronic circuitry and fiber‑optic networks, translating electrical signals into light and vice‑versa with minimal loss. Their role is essential in telecommunications backbones, data center interconnects, enterprise LANs, and emerging use cases such as high‑performance computing and AI‑driven workloads. As operators transition from legacy 10 G solutions to 100 G, 400 G, and beyond, transceiver manufacturers are compelled to balance speed, power efficiency, and form‑factor density.

Download FREE Sample Report:

Optical Transceivers Market - View in Detailed Research Report

Key Growth Catalysts

The surge in data center construction worldwide is the foremost engine driving optical transceiver demand. Hyperscale operators such as Amazon Web Services, Microsoft Azure, and Google Cloud are continuously expanding capacity, adopting higher‑density QSFP‑DD and OSFP modules to meet the bandwidth requirements of AI, machine learning, and real‑time analytics. Simultaneously, the global rollout of 5G networks compels telecom operators to upgrade fronthaul and midhaul links, favoring coherent and PAM4‑based transceivers that can deliver 100 G+ performance over longer distances with lower power consumption.

Another significant factor is the emergence of high‑speed inter‑chip and chip‑to‑board optical interfaces in data‑center servers and networking equipment. The industry’s shift toward silicon photonics enables tighter integration, reduced form factor, and cost efficiencies, allowing OEMs to embed optical modules directly onto system‑in‑package (SiP) solutions. This development is especially pronounced in regions with strong semiconductor ecosystems, where co‑location of design houses and foundries accelerates time‑to‑market.

Regulatory pressure toward energy efficiency and carbon‑neutral data center operations also influences technology selection. Operators are favoring transceivers that deliver lower power per bit (pJ/bit) and support dynamic power scaling, both of which contribute to reduced operational expenditures and compliance with green‑IT standards.

Finally, the proliferation of edge computing - driven by low‑latency needs for IoT, autonomous vehicles, and smart‑city applications - creates a parallel demand stream for compact, rugged optical modules capable of operating in constrained environments while maintaining high reliability.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Optical Transceivers Market Dominated by Top 5 Players Holding 63% Share

The optical transceivers market is highly concentrated with II‑VI (Finisar) and Broadcom (Avago) leading the industry. These companies dominate through technological innovation, extensive product portfolios, and strategic acquisitions. II‑VI strengthened its position through the acquisition of Finisar in 2019, while Broadcom maintains leadership through its high‑speed optical components. The top 5 players collectively control 63% of the global market, with China emerging as the largest regional market.

Beyond the market leaders, several niche players are gaining traction in specialized segments. Companies like Lumentum (Oclaro) excel in high‑performance transceivers for telecom networks, while NeoPhotonics specializes in coherent optical modules. Asian manufacturers such as Accelink and Fujitsu are expanding their presence through competitive pricing and localized supply chains. Emerging applications in data centers and 5G networks are creating opportunities for smaller players to compete in specific technology segments.

List of Key Optical Transceivers Companies Profiled

-

II-VI(Finisar)

-

Lumentum(Oclaro)

-

Sumitomo

-

Accelink

-

Cisco

-

Alcatel-Lucent

-

NeoPhotonics

-

Source Photonics

-

Molex(Oplink)

-

Huawei

-

Infinera(Coriant)

-

ACON

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

100 G Transceivers dominate due to:

|

| By Application |

|

Data Center Segment shows strongest momentum due to:

|

| By End User |

|

Cloud Service Providers lead adoption due to:

|

| By Form Factor |

|

QSFP/QSFP+ maintains strong position because:

|

| By Technology |

|

PAM4 Technology gaining significant traction due to:

|

Regional Analysis: Global Optical Transceivers Market

Hyperscale operators in North America drive massive demand for 400G/800G optical transceivers to support cloud computing and AI workloads. Emerging edge data centers create additional opportunities for compact form factors like QSFP‑DD and OSFP modules.

Accelerated 5G deployments require fronthaul and midhaul optical links, boosting demand for industrial‑grade transceivers. Telecom operators prioritize low‑latency, high‑density optical solutions to support next‑generation mobile networks across urban and rural areas.

Silicon Valley remains the innovation hub for optical networking, with companies developing advanced coherent DSPs and integrated photonic circuits. Ecosystem collaborations between chip designers and module manufacturers accelerate product development cycles.

Strict data sovereignty laws and cybersecurity requirements compel enterprises to upgrade network infrastructure with secure optical transceivers. Government initiatives promote domestic manufacturing of critical optical components to ensure supply chain resilience.

Europe

Europe demonstrates steady growth in optical transceivers adoption, driven by Digital Agenda initiatives focused on fiber‑optic network modernization. The EU's push for open RAN architectures creates new opportunities for interoperable optical components. Leading telecom operators actively deploy 100G+ coherent solutions for metro and long‑haul networks, while enterprise demand grows for cost‑effective pluggable optics. Germany and France emerge as manufacturing hubs for industrial‑grade transceivers, supported by precision engineering capabilities and photonics research clusters. Stringent energy efficiency regulations promote development of low‑power optical modules for sustainable data center operations.

Asia‑Pacific

Asia‑Pacific represents the fastest‑growing optical transceivers market, fueled by massive data center construction in China, Japan, and Singapore. Chinese manufacturers dominate volume production of cost‑competitive transceivers while Japanese companies lead in high‑performance optical components. India's expanding telecom sector drives demand for affordable 10G/25G solutions. Regional governments invest heavily in national broadband networks, creating opportunities for FTTH optical modules. The emergence of hyperscale data center hubs in Jakarta and Mumbai sparks demand for high‑speed interconnects across Southeast Asia.

South America

South America shows growing potential in optical transceivers adoption as Brazilian and Chilean data centers upgrade infrastructure. Submarine cable projects connecting the continent to North America and Europe stimulate demand for long‑haul coherent transceivers. Limited local manufacturing capabilities create import opportunities for international suppliers. Telecom operators prioritize network modernization to support digital transformation initiatives across banking and education sectors. Growing adoption of cloud services drives demand for data center interconnects in major metropolitan areas.

Middle East & Africa

The Middle East experiences robust optical transceivers demand from smart city projects and hyperscale data centres in UAE and Saudi Arabia. African markets gradually adopt optical networking solutions with submarine cable landings driving coastal connectivity. Oil & gas industries deploy industrial‑grade transceivers for harsh‑environment applications. Limited infrastructure in rural areas presents long‑term growth potential for fiber‑optic penetration. Regional telecom operators collaborate with global technology providers to modernise backbone networks.

Get Full Report Here:

Optical Transceivers Market, Trends, Business Strategies 2025-2032 - View in Detailed Research Report

About Semiconductorinsight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us