Automotive LIDAR (Flash, MEMS, FMCW) Chip Market, Trends, Business Strategies 2026-2034

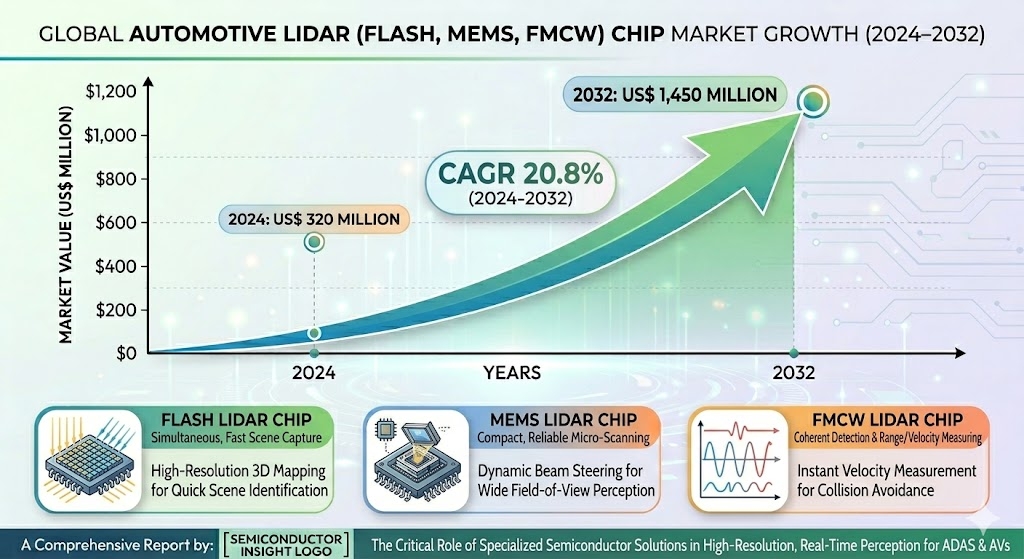

The global Automotive LIDAR (Flash, MEMS, FMCW) Chip Market, valued at a robust US$ 320 million in 2024, is on a trajectory of significant expansion, projected to reach US$ 1,450 million by 2032. This growth, representing a compound annual growth rate (CAGR) of 20.8%, is detailed in a comprehensive new report published by Semiconductor Insight. The study highlights the critical role of these specialized semiconductor solutions in enabling high-resolution, real-time environmental perception for advanced driver assistance systems and autonomous vehicles.

Automotive LIDAR chips, encompassing Flash, MEMS, and FMCW technologies, are becoming indispensable in delivering precise 3D mapping and object detection capabilities. Their compact designs and advanced signal processing features allow for seamless integration into vehicle architectures, minimizing latency and optimizing performance in diverse driving conditions, making them a cornerstone of next-generation mobility solutions.

Download FREE Sample Report:

Automotive LIDAR (Flash, MEMS, FMCW) Chip Market - View in Detailed Research Report

Autonomous Vehicle Revolution: The Primary Growth Engine

The report identifies the rapid advancement toward higher levels of vehicle autonomy as the paramount driver for LIDAR chip demand. With the automotive industry accelerating development of Level 3 and above systems, the need for sophisticated perception hardware continues to intensify. These chips form the core of solid-state LIDAR systems, offering superior reliability compared to traditional mechanical alternatives while supporting the scalability required for mass-market adoption.

"The convergence of Flash, MEMS, and FMCW architectures is reshaping automotive sensing, with each technology addressing specific performance requirements in range, resolution, and velocity measurement," the report states. As global OEMs commit billions to autonomous driving programs and regulatory bodies emphasize safety enhancements, demand for high-performance LIDAR chips is set to intensify, particularly in applications requiring robust operation across varied environmental conditions.

Read Full Report: https://semiconductorinsight.com/report/automotive-lidar-flash-mems-fmcw-chip-market/

Market Segmentation: Technology Diversity Drives Innovation

The report provides a detailed segmentation analysis, offering a clear view of the market structure and key growth segments:

Segment Analysis:

By Type

- Flash LIDAR Chips

- MEMS LIDAR Chips

- FMCW LIDAR Chips

By Application

- Advanced Driver Assistance Systems (ADAS)

- Autonomous Vehicle Navigation

- Object Detection and Mapping

- Others

- Automotive Safety Systems

- Environmental Perception

- Sensor Fusion Platforms

- Others

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Autonomous Shuttles and Robotaxis

Get Full Report Here:

Automotive LIDAR (Flash, MEMS, FMCW) Chip Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

Competitive Landscape: Key Players and Strategic Focus

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive LIDAR (Flash, MEMS, FMCW) Chip Market Competitive Analysis

The Automotive LIDAR chip market for Flash, MEMS, and FMCW technologies is characterized by a dynamic competitive structure dominated by specialized semiconductor innovators and integrated LiDAR system leaders with in-house chip design capabilities. Luminar Technologies stands out as a leading player through its vertical integration strategy, developing proprietary semiconductor components including custom ASICs and photonic integrated circuits optimized for high-performance solid-state LiDAR solutions. The market features a mix of pure-play LiDAR developers advancing application-specific chips and established automotive Tier-1 suppliers leveraging their semiconductor expertise for scalable production. Rapid technological convergence around silicon photonics and advanced signal processing is intensifying competition, with companies focusing on reducing power consumption, enhancing integration, and achieving automotive-grade reliability for mass-market ADAS and autonomous driving applications.

Other significant players include innovators specializing in FMCW coherent detection chips like Aeva, which excels in 4D LiDAR with simultaneous velocity measurement capabilities, alongside MEMS-focused developers such as Hesai Technology and Innoviz Technologies that provide efficient beam-steering semiconductor solutions. Niche contributors are advancing Flash LiDAR architectures and hybrid approaches, supported by collaborations in silicon photonics and photonic integrated circuits. The competitive landscape is further shaped by strategic partnerships between chip designers, LiDAR OEMs, and vehicle manufacturers, driving innovation while addressing cost and performance barriers for broader adoption in Level 3+ autonomous vehicles.

List of Key Automotive LIDAR Chip Companies Profiled

-

Luminar Technologies

-

Innoviz Technologies

-

RoboSense

-

Ouster Inc.

-

Continental AG

-

Cepton Technologies

-

LeddarTech

-

Quanergy Systems

-

Baraja Pty Ltd.

-

Opsys Tech Ltd.

-

Seyond

These companies are focusing on technological advancements, such as enhanced photonic integration and AI-optimized signal processing, alongside geographic expansion into high-growth regions like Asia-Pacific to capitalize on emerging opportunities.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

FMCW LIDAR Chips are gaining prominence for their ability to deliver simultaneous range and velocity measurements through coherent detection. This technology provides superior interference rejection in complex driving environments. It supports robust performance in adverse weather conditions where traditional methods may falter. The integration of advanced signal processing enhances data accuracy for real-time decision making in autonomous systems. |

| By Application |

|

Autonomous Vehicle Navigation represents a critical application area driving innovation in LIDAR chip design. These chips enable precise 3D environmental mapping essential for safe path planning. They facilitate seamless sensor fusion with other vehicle systems for enhanced situational awareness. The demand for high-resolution, real-time data processing pushes continuous improvements in chip efficiency and reliability. |

| By End User |

|

Automotive OEMs are increasingly incorporating these specialized chips to differentiate their vehicle platforms. They prioritize solutions that offer scalability across vehicle models while maintaining automotive-grade reliability standards. Collaboration with chip developers helps tailor solutions to specific platform requirements. This segment emphasizes long-term durability and seamless integration into next-generation vehicle architectures. |

| By Vehicle Type |

|

Passenger Vehicles drive significant demand for compact and cost-effective LIDAR chip solutions. These applications require high-performance sensing in everyday urban and highway scenarios. Manufacturers focus on low-power designs suitable for electric vehicle integration. The emphasis remains on delivering reliable perception capabilities that enhance safety features across diverse driving conditions. |

| By Architecture |

|

Solid-State Solutions are preferred for their durability and lack of moving parts compared to traditional mechanical systems. They enable smaller form factors ideal for seamless vehicle integration. Enhanced semiconductor fabrication techniques improve overall system efficiency and thermal management. This architecture supports the industry shift toward more reliable and scalable autonomous driving technologies. |

Regional Analysis: Automotive LIDAR (Flash, MEMS, FMCW) Chip Market

Asia-Pacific demonstrates superior capabilities in integrating Flash and FMCW LIDAR chip technologies through advanced semiconductor processes. Regional players focus on enhancing detection range and resolution while reducing power consumption, essential for continuous operation in diverse climates. Collaborative R&D efforts drive breakthroughs in hybrid MEMS designs that offer mechanical reliability with solid-state efficiency.

The region benefits from vertically integrated supply chains that streamline production of Automotive LIDAR (Flash, MEMS, FMCW) Chip components. Strong partnerships between wafer fabrication facilities and automotive Tier-1 suppliers ensure consistent quality and rapid iteration. This ecosystem supports cost-effective scaling necessary for widespread adoption across mid-to-premium vehicle segments.

Rapid urbanization and supportive policies propel demand for advanced driver assistance systems incorporating sophisticated LIDAR chips. Local manufacturers prioritize solutions that address challenging traffic scenarios and environmental factors unique to Asian markets, fostering tailored innovations in beam steering and signal processing technologies.

Strategic investments in next-generation fabrication and talent development ensure sustained leadership. The focus remains on achieving higher levels of vehicle autonomy through refined Flash, MEMS, and FMCW LIDAR chip performance, solidifying Asia-Pacific's pivotal role in global automotive transformation.

North America

North America exhibits strong innovation momentum in the Automotive LIDAR (Flash, MEMS, FMCW) Chip Market, particularly through pioneering research in Silicon Valley and automotive hubs across the United States and Canada. The region emphasizes software-hardware co-design for enhanced perception capabilities, with companies focusing on robust FMCW architectures suitable for complex urban environments. Strategic collaborations between technology startups and established automakers accelerate the commercialization of high-resolution LIDAR chips. Regulatory frameworks promoting vehicle safety further encourage integration of advanced sensing solutions, while the presence of leading semiconductor design expertise supports rapid prototyping and customization for premium autonomous platforms.

Europe

Europe maintains a significant position in the Automotive LIDAR (Flash, MEMS, FMCW) Chip Market, driven by stringent safety regulations and a legacy of automotive engineering excellence in Germany, France, and other key nations. The region prioritizes reliability and compliance in MEMS and Flash LIDAR chip development, aligning with comprehensive ADAS and autonomous driving standards. European manufacturers focus on sustainable production methods and seamless integration with existing vehicle architectures. Cross-border initiatives foster knowledge sharing, enhancing capabilities in environmental perception technologies crucial for all-weather performance in varied European climates.

South America

South America is gradually emerging in the Automotive LIDAR (Flash, MEMS, FMCW) Chip Market, with Brazil and other countries exploring opportunities through technology transfer and localized assembly. The focus centers on adapting global LIDAR solutions to regional infrastructure challenges and cost-sensitive markets. Growing interest in smart mobility solutions encourages partnerships that introduce MEMS-based systems for entry-level autonomous features. While infrastructure development remains key, increasing investments in electric vehicles create a foundation for future demand of affordable LIDAR chip technologies tailored to local transportation needs.

Middle East & Africa

The Middle East and Africa region shows promising potential in the Automotive LIDAR (Flash, MEMS, FMCW) Chip Market, particularly in Gulf countries investing in futuristic smart cities and autonomous transport initiatives. Efforts concentrate on deploying robust FMCW LIDAR chips capable of handling extreme environmental conditions like high temperatures and dust. Strategic vision programs in nations such as the UAE drive adoption of advanced sensing technologies. Africa presents opportunities through urban mobility projects, with emphasis on cost-effective solutions that can support gradual implementation of LIDAR-enabled safety systems across developing transportation networks.

Emerging Opportunities in Autonomous Mobility and Smart Cities

Beyond traditional drivers, the report outlines significant emerging opportunities. The rapid expansion of robotaxi services, autonomous trucking, and smart city infrastructure presents new growth avenues, requiring sophisticated LIDAR chip solutions for reliable operation. Furthermore, the integration of AI and edge computing is a major trend. Advanced chips with embedded processing capabilities can significantly enhance real-time decision-making while optimizing power efficiency in electric vehicle platforms.

Report Scope and Availability

The market research report offers a comprehensive analysis of the global and regional Automotive LIDAR (Flash, MEMS, FMCW) Chip markets from 2025–2032. It provides detailed segmentation, market size forecasts, competitive intelligence, technology trends, and an evaluation of key market dynamics.

For a detailed analysis of market drivers, restraints, opportunities, and the competitive strategies of key players, access the complete report.

Read Full Report: https://semiconductorinsight.com/report/automotive-lidar-flash-mems-fmcw-chip-market/

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=142703

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data-driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us