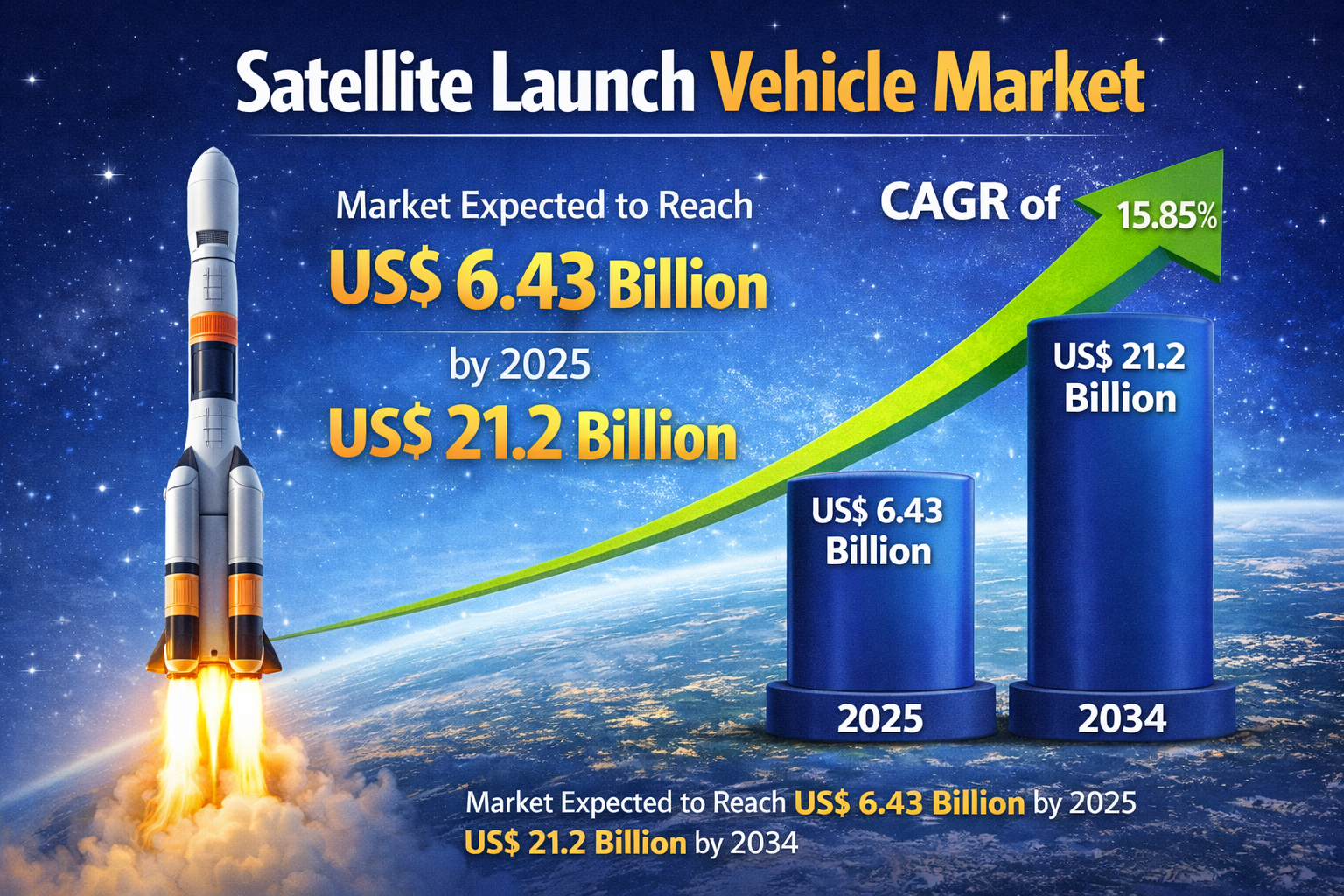

From US$ 6.43 Billion in 2025 to US$ 21.2 Billion by 2034: The Rapid Rise of the Satellite Launch Vehicle Industry

A Satellite Launch Vehicle (SLV) is a powerful rocket system used to place satellites and other payloads into orbit around Earth. It enables key space applications such as communication networks, GPS navigation, earth monitoring, meteorology, research missions, and defense activities.

Satellite Launch Vehicle Market Share, Size and Future Opportunities 2034

The Satellite Launch Vehicle Market is experiencing robust expansion, fueled by rising satellite deployments, commercial space exploration, and government-backed space programs. According to industry analysis, the market size is projected to reach US$ 6.43 Billion in 2025 and is anticipated to grow significantly to US$ 21.2 Billion by 2034, registering a strong CAGR of 15.85% during the forecast period (2026–2034). The growing integration of satellite technologies across communication, navigation, meteorology, earth observation, and scientific research is driving consistent demand for reliable and cost-effective launch services.

Market Overview

Satellite launch vehicles play a critical role in placing payloads into various orbits, including Sun-Synchronous Orbit (SSO), Medium Earth Orbit (MEO), Low Earth Orbit (LEO), and Geosynchronous Orbit (GEO). Among these, LEO deployments are witnessing substantial growth due to the increasing adoption of small satellite constellations for broadband connectivity and earth observation applications. Meanwhile, GEO remains essential for communication and broadcasting satellites.

By launch activity, the market is segmented into Commercial and Non-Commercial launches. The commercial segment is expanding rapidly as private players increase participation in satellite deployment services. Government space agencies continue to contribute significantly through non-commercial missions, including defense, scientific exploration, and research-based initiatives.

Applications covered in the report include Research & Development, Navigation, Communication, Scientific, Meteorology, Earth Observation, and Remote Sensing. The communication segment dominates the market due to rising demand for global connectivity, 5G infrastructure support, and broadband internet services. Additionally, navigation and earth observation applications are gaining momentum due to advancements in geospatial technologies and climate monitoring systems.

Request Sample PDF Here: https://www.theinsightpartners.com/sample/TIPRE00007920

Regional Insights

The market demonstrates strong regional diversification across North America, Europe, Asia-Pacific, South & Central America, and the Middle East & Africa.

-

North America leads the global market, supported by technological innovation, private-sector investment, and established aerospace infrastructure.

-

Asia-Pacific is expected to witness the fastest growth, driven by increasing investments from China, India, and Japan in satellite technology and launch capabilities.

-

Europe maintains steady expansion through collaborative space initiatives and commercial satellite programs.

Growing national security concerns, digital transformation initiatives, and increasing reliance on satellite-enabled services are further strengthening global demand.

Market Drivers and Opportunities

The surge in satellite constellations for broadband connectivity and IoT applications has significantly increased launch frequency requirements. Additionally, government investments in deep-space missions and planetary exploration programs continue to boost demand for heavy-lift and hybrid launch vehicles.

Emerging opportunities include:

-

Development of small satellite dedicated launch services

-

Advancements in reusable launch systems to reduce costs

-

Integration of hybrid propulsion technologies

-

Increased commercialization of space operations

These advancements are improving cost efficiency, mission flexibility, and operational scalability across the industry.

Key Market Players

The competitive landscape features a mix of established aerospace giants and emerging private launch service providers. Key companies include:

-

ARCA Space

-

Blue Origin

-

Boeing Space and Communication

-

E Prime Aerospace

-

ISRO

-

Kelly Space and Technology

-

Lockheed Martin

-

Mitsubishi Heavy Industries

-

SpaceX

-

Virgin Galactic

These companies focus on technological innovation, reusable systems, strategic partnerships, and global expansion to strengthen their market position. Growing competition is fostering cost optimization and faster mission turnaround times.

Future Outlook

The future of the Satellite Launch Vehicle Market appears highly promising, with rapid commercialization of space activities reshaping industry dynamics. The expansion of satellite mega-constellations, advancements in reusable and hybrid launch technologies, and increasing public-private partnerships are expected to drive sustained growth through 2034. As global connectivity demands rise and governments continue investing in space exploration and defense capabilities, the market is set to become a cornerstone of the evolving space economy. With a projected value of US$ 21.2 Billion by 2034, the industry is poised for transformative growth, innovation, and expanded accessibility to space services worldwide.

Related Reports: