Global Nuclear Grade Zirconium Material Market to Reach USD 125.56 Million by 2034 at 5.1% CAGR

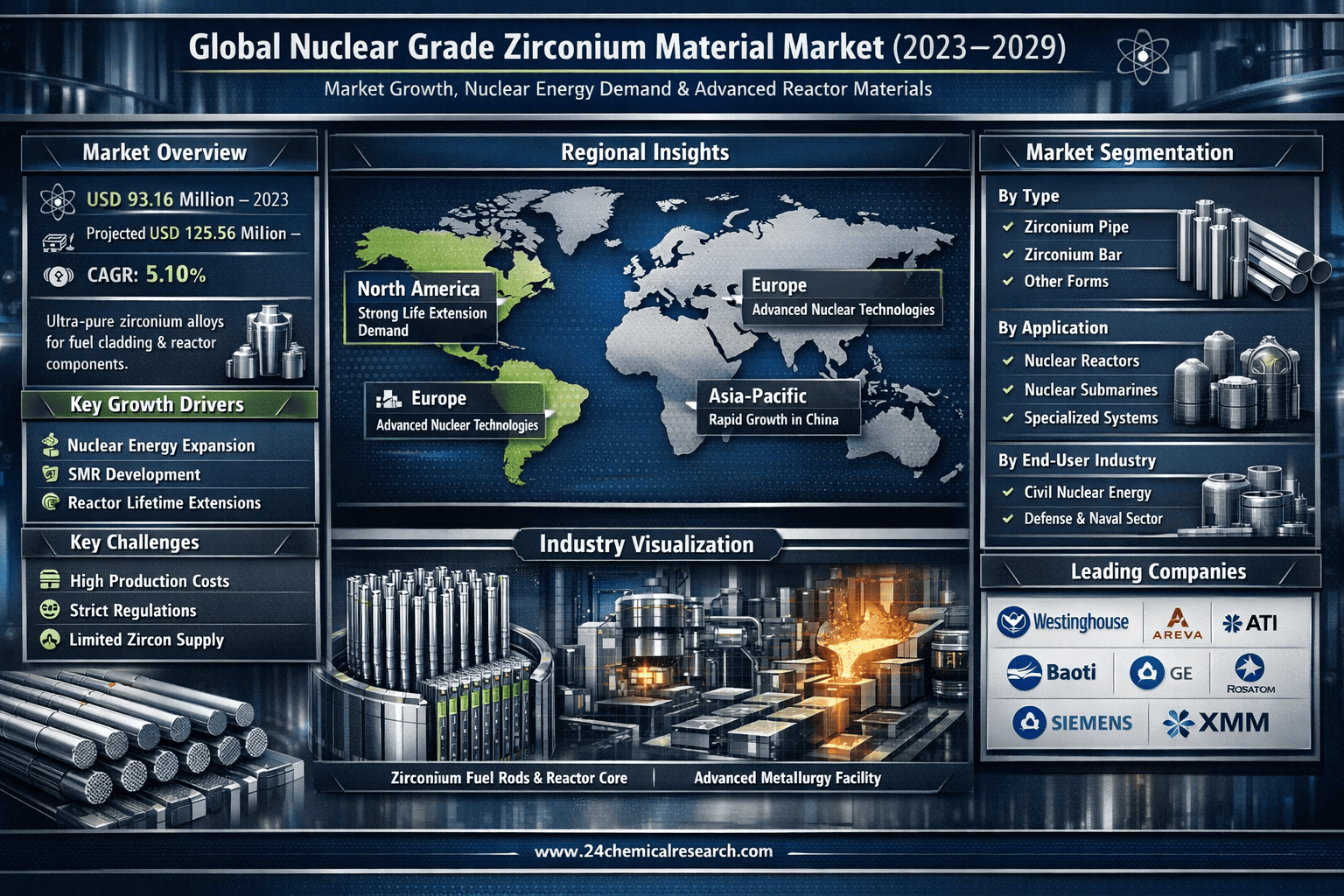

According to 24Chemical Research, Global Nuclear Grade Zirconium Material market was valued at USD 93.16 million in 2023 and is projected to reach USD 125.56 million by 2029, exhibiting a CAGR of 5.10% during the forecast period.

Nuclear Grade Zirconium Material, a specialized class of zirconium alloys characterized by their exceptionally low hafnium content and neutron transparency, has evolved from a niche engineering material to become the backbone of modern nuclear energy infrastructure. Its unique properties—including exceptional corrosion resistance, high-temperature mechanical strength, and minimal neutron absorption cross-section—make it indispensable for nuclear applications. Unlike commercial grade zirconium, nuclear grade material undergoes rigorous purification and quality control processes, ensuring its performance under extreme radiation and thermal conditions within reactor cores.

Get Full Report Here: https://www.24chemicalresearch.com/reports/264225/global-nuclear-grade-zirconium-material-market-2024-589

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

-

Global Nuclear Energy Renaissance: The integration of nuclear grade zirconium in fuel cladding, pressure tubes, and core structural components represents the fundamental growth vector. The global nuclear energy industry, with over 440 operational reactors worldwide, is experiencing renewed investment as nations seek carbon-free baseload power. Recent commitments to nuclear power from countries like China, which has 21 new reactors under construction, and policy shifts in Japan and Europe toward nuclear restarts create sustained demand. Each new reactor requires approximately 20-30 metric tons of zirconium alloy components, creating a direct correlation between nuclear expansion and material demand.

-

Fleet Lifetime Extension Programs: The nuclear sector is undergoing extensive life extension initiatives, with many reactors approved for operation beyond their original 40-year design life. These programs require extensive component replacement and refurbishment, particularly of zirconium alloy fuel assemblies and core internals. With over 90 reactors in the United States alone having received license extensions to 60 years, and similar trends globally, this represents a substantial aftermarket opportunity. Replacement fuel assemblies for a single reactor can represent orders of 15-20 metric tons of nuclear grade zirconium every 18-24 months during refueling cycles.

-

Advanced Reactor Technologies: Next-generation reactor designs including small modular reactors (SMRs) and Generation IV systems are creating new application avenues. These designs often incorporate zirconium alloys in innovative configurations and require material with even stricter specifications. The global SMR market, with projects advancing in the United States, Canada, and the United Kingdom, represents a potential demand for thousands of metric tons of specialized zirconium products over the next decade as these reactors move from demonstration to commercialization.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/264225/global-nuclear-grade-zirconium-material-market极速赛车开奖结果查询 10-599

Significant Market Restraints Challenging Adoption

Despite its critical importance, the market faces hurdles that must be overcome to achieve optimal growth.

-

Extreme Production Complexity and Cost Structure: The sophisticated manufacturing processes required to produce nuclear grade zirconium, involving multiple stages of purification, alloying, and forming, involve specialized equipment and controlled environments. This elevates production costs by 300-400% above those of conventional zirconium products. The multi-step purification process to achieve hafnium content below 100 ppm requires specialized chemical processing equipment and adds significant time and cost to production cycles, creating economic barriers for new market entrants.

-

Stringent Regulatory and Certification Requirements: In the nuclear sector, the path to regulatory qualification for materials is exceptionally rigorous and time-consuming. Current certification timelines for new material grades or production facilities can extend from 3 to 5 years in major nuclear markets. The ongoing requirements for nuclear quality assurance programs (NQA-1 standards in the U.S., ISO 19443 internationally) create continuous compliance costs that represent 8-12% of annual revenue for material producers, potentially limiting innovation and market participation.

Critical Market Challenges Requiring Innovation

The transition from laboratory development to industrial-scale nuclear qualification presents its own set of challenges. Maintaining material consistency at production volumes exceeding 500 metric tons annually is difficult, with current processes requiring 100% destructive testing of samples from every production batch. Furthermore, ensuring dimensional stability and material properties through complex fabrication processes like pilgering and welding is problematic, with rejection rates of 15-20% for finished components. These technical hurdles necessitate massive quality assurance investments, often consuming 20-25% of production costs, creating significant barriers to entry.

Additionally, the market contends with a highly specialized and consolidated supply chain. Dependency on a limited number of zircon sand mining operations worldwide and the added complexity of securing nuclear-grade hafnium-free feedstocks create supply vulnerability. The transportation and storage of nuclear-grade materials also involves additional security and documentation requirements that add 7-10% to logistics costs compared to industrial materials.

Vast Market Opportunities on the Horizon

-

Nuclear Fuel Cycle Innovation: Advanced fuel designs including accident-tolerant fuel (ATF) cladding represent a potential transformation in nuclear safety technology. Zirconium alloys enhanced with chromium or other coatings demonstrate dramatically improved oxidation resistance during accident scenarios. With the global nuclear fuel market valued at approximately $12 billion annually, these advanced cladding technologies, which have demonstrated 5-10 times better oxidation resistance in test reactors, are poised to become standard in the industry within the next decade.

-

Nuclear Navy and Specialized Applications: Naval nuclear propulsion programs continue to represent a stable and technically demanding market segment. The requirement for compact, high-performance reactor systems for aircraft carriers and submarines drives innovation in zirconium alloy development. These applications often pioneer advanced material technologies that later transition to civilian nuclear programs, creating a virtuous cycle of innovation and application expansion.

-

International Collaboration as Growth Catalyst: The market is witnessing increased international partnership activity. Strategic collaborations between Western technology providers and emerging nuclear programs in countries like the United Arab Emirates, Turkey, and Poland are facilitating technology transfer and market expansion. These partnerships are crucial for establishing new supply chains and qualifying local production capabilities, effectively reducing geopolitical supply risks and creating more resilient market structures.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Zirconium Pipe, Zirconium Bar, and other forms. Zirconium Pipe currently leads the market, favored for its critical application as fuel cladding tubing and pressure tubes in various reactor designs. The precise dimensional tolerances and material properties required for these applications make them the most technically demanding and valuable product form. Bar stock is essential for manufacturing components like spacer grids and structural supports within reactor cores.

By Application:

Application segments include Nuclear Reactor, Nuclear Submarine, and other specialized nuclear applications. The Nuclear Reactor segment overwhelmingly dominates, driven by the continuous global demand for civilian nuclear power generation components. However, the specialized naval nuclear segment maintains consistent demand for high-performance materials and represents an important sector for advanced material development and testing.

By End-User Industry:

The end-user landscape is concentrated in the Energy sector, with specialized applications in Defense for naval propulsion. The Civil Nuclear Energy industry accounts for the major share, leveraging zirconium's properties for fuel assemblies, core internals, and other critical components. The Defense sector represents a smaller but technically sophisticated market segment with demanding specifications and long-term procurement cycles.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/264225/global-nuclear-grade-zirconium-material-market-2024-589

Competitive Landscape:

The global Nuclear Grade Zirconium Material market is highly consolidated and characterized by significant barriers to entry and long qualification cycles. The top three companies—Westinghouse Electric (U.S.), AREVA (France), and State Nuclear Baoti Zirconium Industry (China)—collectively command approximately 70% of the market share as of 2023. Their dominance is underpinned by extensive intellectual property portfolios, vertically integrated production capabilities, and established relationships with nuclear plant operators worldwide.

List of Key Nuclear Grade Zirconium Material Companies Profiled:

-

Westinghouse Electric (U.S.)

-

AREVA (France)

-

极速赛车开奖号码查看 59

-

ATI (U.S.)

-

State Nuclear Baoti Zirconium Industry (China)

-

General Electric (U.S.)

-

RosEnergoAtom (Russia)

-

Siemens (Germany)

-

Xian Western Energy Material (China)

The competitive strategy is overwhelmingly focused on maintaining nuclear quality assurance standards, continuous process improvement to reduce costs, and developing long-term supply agreements with utility customers to secure stable demand over multi-year horizons.

Regional Analysis: A Global Footprint with Distinct Leaders

-

North America and Europe: Together form the established leader, holding a 55% share of the global market. This dominance is fueled by extensive nuclear fleets, mature regulatory frameworks, and strong technological capabilities. The United States and France are the primary engines of demand in these regions, supported by ongoing life extension programs and commitments to maintaining nuclear energy capacity.

-

Asia-Pacific: Represents the rapidly growing segment, accounting for 40% of the market. China's ambitious nuclear expansion program, with multiple reactors under construction, drives much of this growth. South Korea and Japan maintain significant nuclear capabilities and continue to represent important markets despite varying energy policy challenges.

-

Other Regions: These areas represent emerging opportunities driven by new nuclear programs. Countries in the Middle East, Eastern Europe, and Southeast Asia considering or initiating nuclear power programs present long-term growth potential as they establish their nuclear infrastructure and supply chains.

Get Full Report Here: https://www.24chemicalresearch.com/reports/264225/global-nuclear-grade-zirconium-material极速赛车预测软件推荐 2024-589

Download FREE极速赛车开奖结果官方网站 Sample Report: https://www.24chemicalresearch.com/download-sample/264225/global-nuclear-grade-zirconium-material-market-202极速赛车开奖结果查询 10-589

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key极速赛车开奖结果直播 industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring极速赛车开奖结果历史记录

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/