Growing Health Trends Fuel Non-Alcoholic Wine Market to USD 7.64 Billion

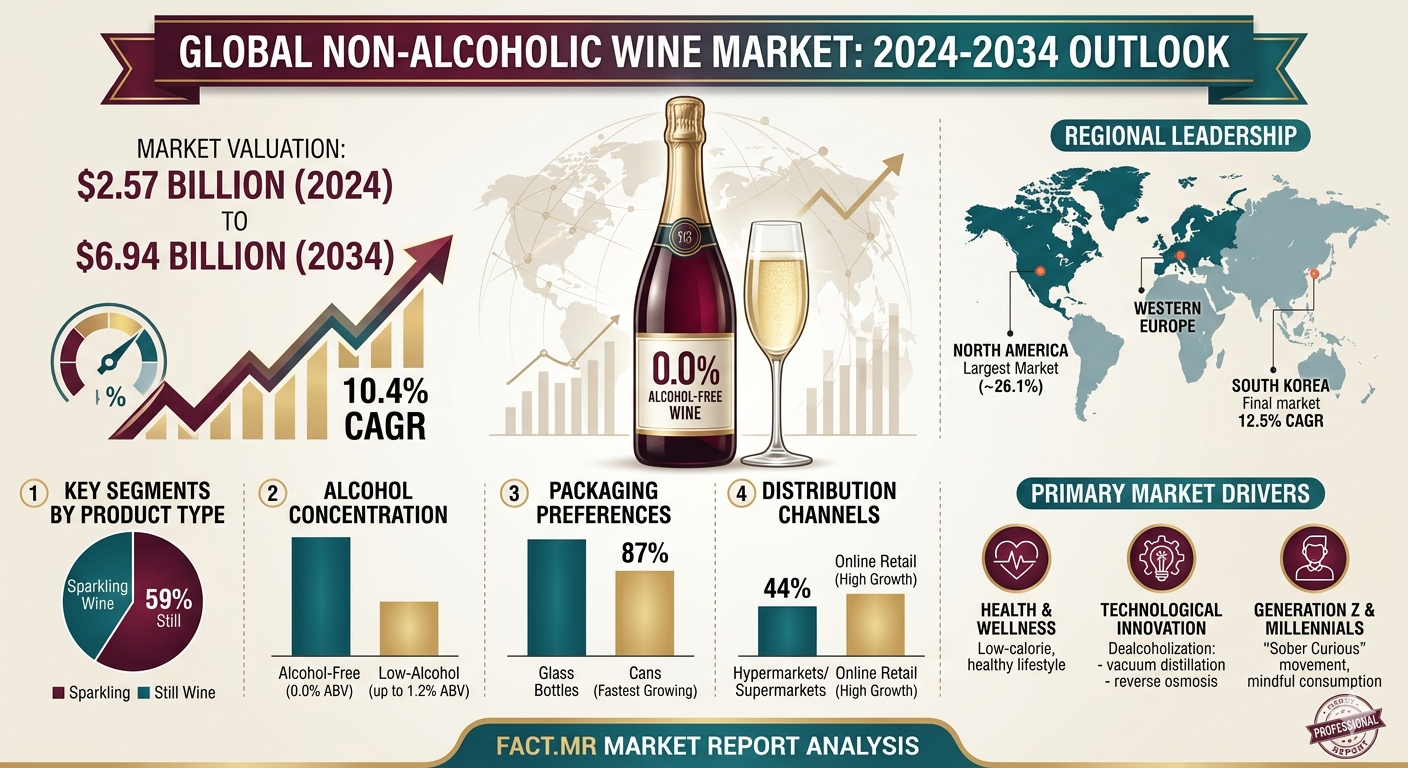

The global non-alcoholic wine market is positioned for a decade of high-velocity growth, with its valuation expected to rise from USD 2.84 billion in 2025 to USD 7.64 billion by 2035. This expansion, occurring at a compound annual growth rate (CAGR) of 10.4%, is fueled by a profound shift toward "sober-curious" lifestyles and the integration of advanced dealcoholization technologies that preserve the sensory integrity of traditional vintages.

Get Aceess Report Sample : https://www.factmr.com/connectus/sample?flag=S&rep_id=4532

Non-Alcoholic Wine Market Quick Stats

- Market Size (2025): USD 2.84 billion.

- Market Size (2035): USD 7.64 billion.

- Compound Annual Growth Rate (CAGR): 10.4% (2025–2035).

- Leading Product Segment: Sparkling wine is the most profitable category, projected to grow at a 9.2% CAGR.

- Leading Alcohol Concentration: Alcohol-free products (0.0% ABV) lead the industry with a projected 9.5% CAGR.

- Fastest Growing Packaging: Cans are expected to register an 8.9% CAGR due to portability and sustainability.

- Top Sales Channel: Online stores are the dominant distribution leader with a 10.1% CAGR.

- Key Growth Regions: North America, Western Europe, East Asia, and South Asia & Pacific.

- Top Companies: Ariel Vineyards, Fre Alcohol-Removed Wines, Pierre Zéro (Pernod Ricard), Lussory Non-Alcoholic Wines, Eisberg, and Töst

Market Momentum (YoY Path)

The non-alcoholic wine industry is navigating a consistent upward trajectory. Following a strong 2024 close at USD 2.57 billion, the market is anticipated to reach USD 2.84 billion in 2025. Strategic investments in flavor preservation and functional ingredients are expected to push the valuation to approximately USD 3.75 billion by 2028 and USD 4.56 billion by 2030. By 2031, the industry is forecasted to cross the USD 5.04 billion mark. Sustained momentum in digital retail and premiumization will drive the value to USD 6.18 billion by 2033, ultimately culminating in a total market size of USD 7.64 billion by 2035.

Why the Market is Growing

The primary catalyst for the Non-Alcoholic Wine Market is a global transition toward health-conscious consumption. Consumers in urban centers are increasingly seeking alternatives to traditional alcohol that offer the same sophisticated flavor profiles without the health risks. This is further supported by technological breakthroughs like vacuum distillation and reverse osmosis, which allow winemakers to remove alcohol while retaining delicate aromas. Additionally, cultural momentum in the Middle East and Southeast Asia, where religious or legislative alcohol prohibitions exist, provides a massive untapped audience for zero-proof wine substitutes.

Segment Spotlight

Product Type: Sparkling vs. Still

The Sparkling wine category is the industry’s standout performer. Valued for its association with celebratory events, it appeals heavily to Millennials and Gen Z who view sparkling variants as a bridge between wellness and sophistication. This segment's growth outpaces the broader market as brands innovate with low-calorie and fruit-forward profiles.

Alcohol Concentration: The Rise of Alcohol-Free

The Alcohol-Free segment is projected to grow at a 9.5% CAGR, outperforming the industry benchmark. Driven by government-sponsored sobriety campaigns and a rising population of abstainers, these 0.0% ABV products are seeing massive scalability due to their acceptance in religious and wellness communities worldwide.

Packaging: The Shift to Cans

While glass bottles remain traditional, Cans are the fastest-growing packaging format at an 8.9% CAGR. This shift is driven by urban "on-the-go" consumption patterns, the demand for better portion control, and increasingly stringent recycling laws that favor sustainable aluminum over traditional glass.

Drivers, Opportunities, Trends, and Challenges

Drivers: The core driver is the "clean label" movement and the normalization of social zero-proof consumption. Increasing health awareness and the availability of premiumized options in retail chains have made non-alcoholic wine a mainstream lifestyle choice rather than a niche medical requirement.

Opportunities: There is a significant opportunity in functional additives. Integrating adaptogens, botanicals, and antioxidants into wine formulations allows brands to differentiate themselves by offering "wellness in a glass." Furthermore, expansion into digital-first Direct-to-Consumer (DTC) models provides a streamlined path to global audiences.

Trends: AI-facilitated fermentation and flavor profiling are redefining product development. In the U.S., brands are focusing on organic certification and single-serve formats, while in South Korea, "ginseng-infused" and "skin-improving" blends are merging the boundaries between indulgence and functional health.

Challenges: The industry faces hurdles such as non-uniform global labeling standards and high input prices for organic grapes. Cultural unfamiliarity in markets like Japan and India can slow adoption, while high import tariffs in India remain a barrier for international premium brands.

Country Growth Outlook (CAGR 2025–2035)

|

Country |

Projected CAGR |

Key Market Influence |

|

China |

7.1% |

Middle-class growth and traditional herb infusions. |

|

India |

6.8% |

Urban millennial demand and Tier-1 city expansion. |

|

South Korea |

6.4% |

AI-optimized personalization and wellness culture. |

|

Australia-NZ |

6.2% |

Public health storytelling and sustainability. |

|

Germany |

6.1% |

Advanced dealcoholization and clean labeling. |

|

United Kingdom |

5.6% |

Pub demand and sustainable local sourcing. |

|

USA |

5.2% |

Premiumization and big-box retail expansion. |

|

France |

5.4% |

Terroir-style low-alcohol practices in city centers. |

Competitive Landscape

The Non-Alcoholic Wine Market is a fragmented landscape where global beverage giants compete with artisanal specialty brands. Ariel Vineyards currently holds a dominant 20-25% share, particularly in North America. Fre Alcohol-Removed Wines follows with a 15-20% share, leveraging the scale of the Sutter Home portfolio. Pierre Zéro (Pernod Ricard) maintains a 10-15% share by focusing on luxury hospitality. Other significant players include Lussory Non-Alcoholic Wines, Eisberg, Töst, Giesen Wines, and Treasury Wine Estates. These companies are increasingly utilizing spinning cone technology and AI-driven supply chains to maintain a competitive edge.

To View Related Reports

Swine Feed Market https://www.factmr.com/report/290/swine-feed-market

Red Wine Industry Analysis in the UK https://www.factmr.com/report/united-kingdom-red-wine-industry-analysis

Red Wine Market https://www.factmr.com/report/160/red-wine-market

CBD Wine Market https://www.factmr.com/report/cbd-wine-market

- Contact Us -

11140 Rockville Pike, Suite 400, Rockville,

MD 20852, United States

Tel: +1 (628) 251-1583 | sales@factmr.com

About Fact.MR

Fact.MR is a global market research and consulting firm, trusted by Fortune 500 companies and emerging businesses for reliable insights and strategic intelligence. With a presence across the U.S., UK, India, and Dubai, we deliver data-driven research and tailored consulting solutions across 30+ industries and 1,000+ markets. Backed by deep expertise and advanced analytics, Fact.MR helps organizations uncover opportunities, reduce risks, and make informed decisions for sustainable growth.